Entrepreneurship and Fiscal Policy – How Taxes Affect Entrepreneurial Activity

Many try to divorce entrepreneurship from any fiscal questions, claiming that entrepreneurship is basically a passion, and that entrepreneurs start businesses out of love. Yet one of the fundamental aspects of economic analysis is that cost variations are a primary factor in accounting for human behaviour. Having said this, it is far from obvious which public policies really stimulate entrepreneurship and reduce the cost of starting a business. This paper aims to provide a frank, open discussion of the fiscal measures that affect entrepreneurship.

Media release: High taxes kill entrepreneurship

Related Content

Related Content

|

|

|

| More taxes, less innovation (Toronto Sun, September 17, 2018)

L’amour n’est pas plus fort que l’impôt (Huffington Post Québec, September 14, 2018) |

This Research Paper was prepared by Mathieu Bédard, Economist at the MEI, in collaboration with Kevin Brookes, Public Policy Analyst at the MEI.

Highlights

Many try to divorce entrepreneurship from any fiscal questions, claiming that entrepreneurship is basically a passion, and that entrepreneurs start businesses out of love. Yet one of the fundamental aspects of economic analysis is that cost variations are a primary factor in accounting for human behaviour. Having said this, it is far from obvious which public policies really stimulate entrepreneurship and reduce the cost of starting a business. This paper aims to provide a frank, open discussion of the fiscal measures that affect entrepreneurship.

Chapter 1 – The Ineffectiveness of Business Creation Subsidies

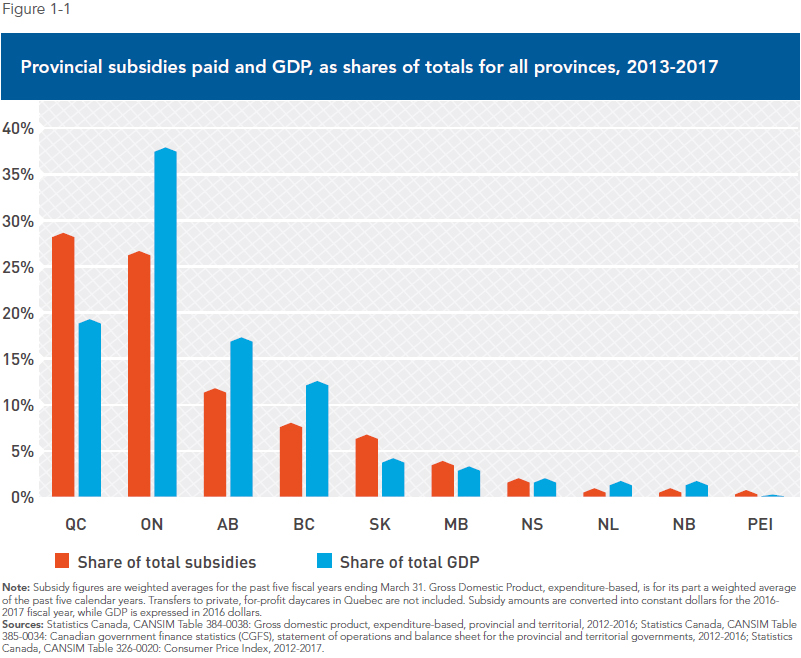

- Canadian companies have access to a multitude of subsidies that can take several forms, including transfer expenditures, tax credits, loans and portfolio investments, and loan guarantees.

- Supporting the economy with subsidies is not a magic bullet, since the taxes used to finance them create distortions in the economy and encourage behaviours that are not socially optimal.

- The existence of subsidies gives rise to “rent seeking,” as entrepreneurs have an incentive to use resources to attempt to receive their share, while politicians have an incentive to use subsidies to increase their chances of being re-elected.

- Governments around the world nonetheless continue to subsidize the creation of businesses because there is a consensus regarding the link between entrepreneurship and job creation, among other desirable economic phenomena.

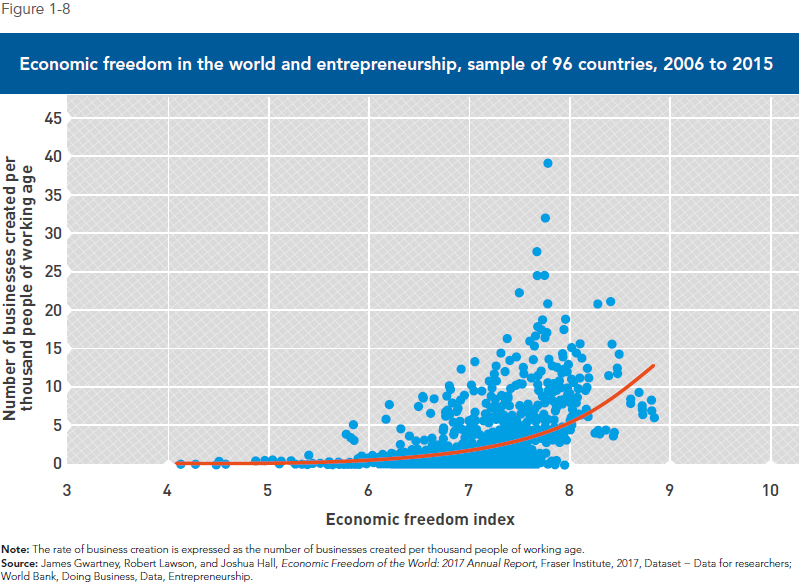

- Yet an increase in the supply of funding available is not necessarily an effective public policy for growing the number of businesses, since it seems that it is entrepreneurial activity that attracts additional venture capital, and not the other way around.

- Those who favour subsidies for business creation and expansion sometimes invoke market failures and externalities, but arguments based on such phenomena are not persuasive.

- If we look at the effect of subsidies to private businesses on the rate of business creation, we see that there is no notable effect, and there even seems to be an inverse relationship, although the variable is not statistically significant.

- It is an entrepreneur’s own personal savings that constitute the most important source of initial funding for Canadian businesses, with 70.5% of start-up capital coming from entrepreneurs’ personal funds in 2015.

- If governments want to encourage the appearance of more entrepreneurial opportunities, and want these to give rise to productive businesses, it would be better off considering public policies to foster competition, lower taxes, the opening up of borders, and a light regulatory burden.

Chapter 2 – The Decision to Start a Business: The Impact of Taxation

- Everyone recognizes that entrepreneurial passion is an essential prerequisite to starting a business, but one of the first lessons of economics is that incentives, including taxation, are crucial in explaining decisions.

- When an entrepreneur chooses to start a business, he or she renounces a career, sometimes as an employee or maybe even as an executive in an established company, and also renounces the salary that goes with this career.

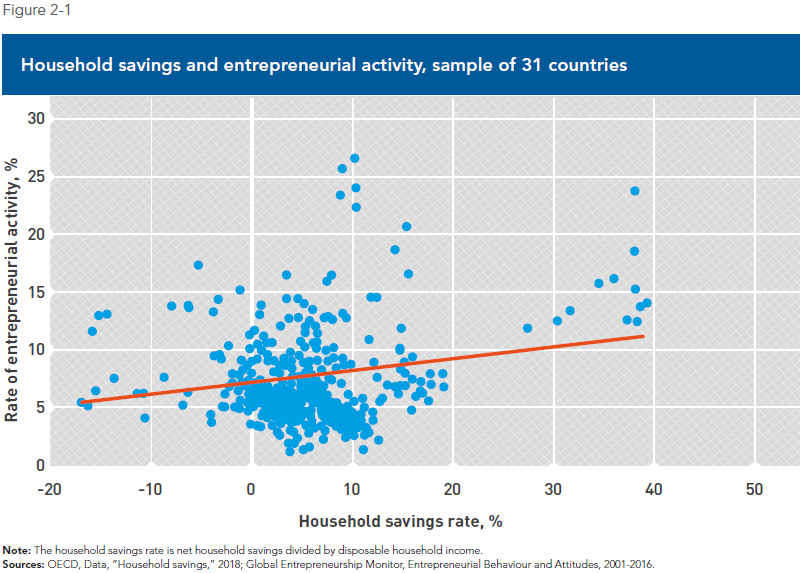

- Before a potential entrepreneur even poses the question of whether to set off on an entrepreneurial adventure, an important factor comes into play, and this factor is in turn heavily influenced by taxation: the accumulation of capital.

- Convincing investors to participate in a project whose importance and potential only the entrepreneur sees can be a very difficult task, which is why the personal accumulation of wealth is crucial.

- The cost of saving is the immediate consumption that one must forego, and taxation increases this cost, in addition to reducing the amount of resources that could be invested.

- In Canada, net household saving, as a percentage of disposable income, has fallen over time, the consequence not only of taxation, but also of the aging of the population and of very low interest rates, among other things.

Chapter 3 – Progressive Taxation and the Self-Employed Worker

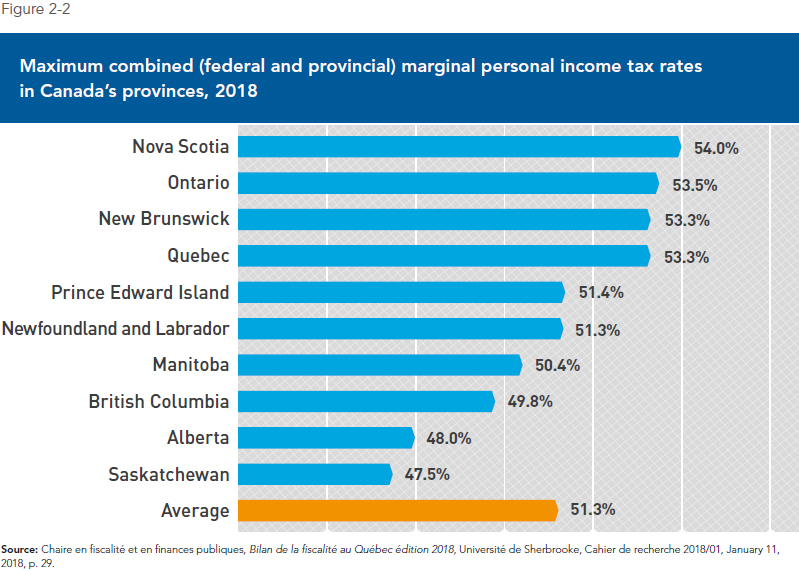

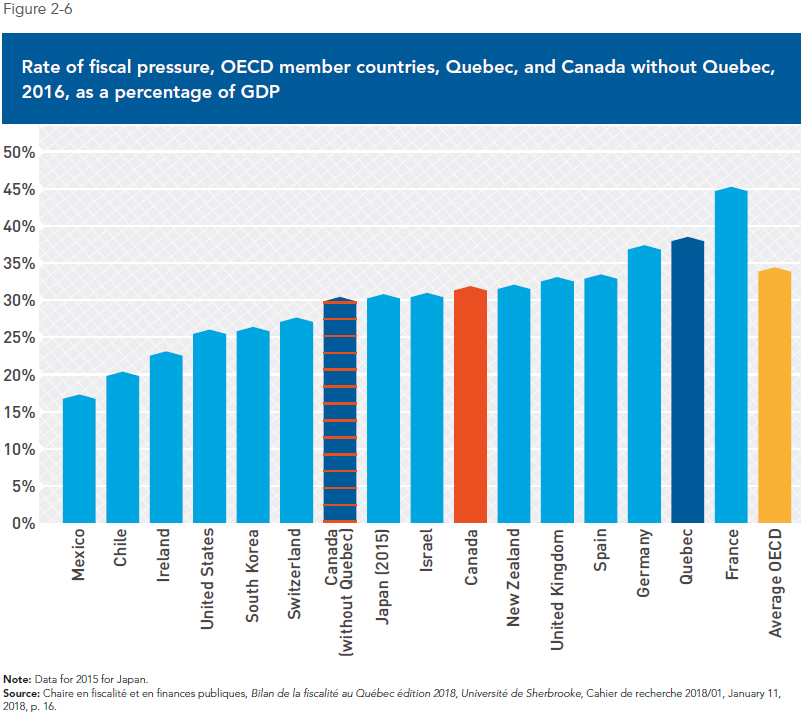

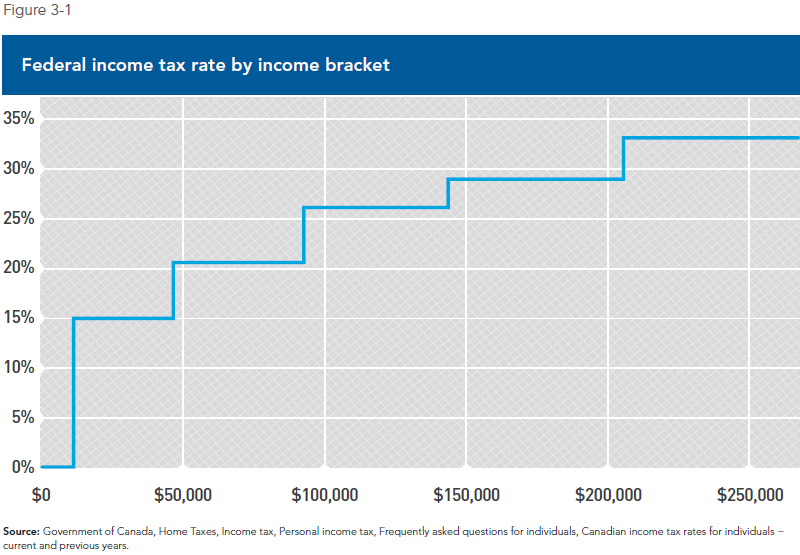

- Comparisons of the progressivity of taxes in industrialized countries show that taxation in Canada is more progressive than in most OECD countries.

- As opposed to progressive taxation, other taxes are called “proportional.” In this case, the same rate applies regardless of income: The amount of tax paid is always the same proportion of income.

- Certain mathematical economists believe that the best tax of all is one that involves a lump sum payment, sometimes called a head tax, but this scenario is inapplicable for political reasons.

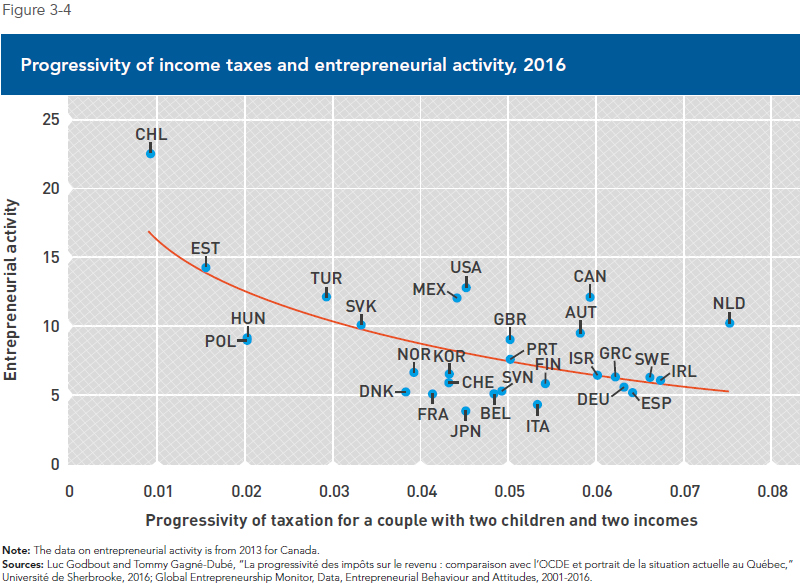

- The more progressive the tax rate is, the more it discourages additional effort, saving, and investment, and therefore ultimately entrepreneurship.

- Countries like Chile and Estonia, whose tax systems are among the least progressive in the world, have more entrepreneurial activity than the OECD countries with more progressive income tax systems.

- In certain very specific cases, taxes can increase entrepreneurship by creating tax advantages in favour of self-employment, for example, but the gain for society, namely the entrepreneur’s solution to a problem, is thus negligible or nonexistent.

Chapter 4 – The Effect of the Capital Gains Tax

- Just as sin taxes reduce the behaviour that is being targeted, the capital gains tax hinders capital formation, which is one of the basic foundations of all economic growth and a necessary precondition to most entrepreneurial projects.

- Capital gains taxation also encourages people to lock in their investments, which hurts economic growth by discouraging the reallocation of capital to its most productive uses.

- The capital gains tax also affects which businesses capitalists invest in, reducing the willingness of investors to finance riskier business start-ups and leading them to prefer less innovative forms of entrepreneurship.

- When this tax is high compared to the taxation of salaries, whether because of a high inclusion rate, a high base rate, or some other factor, it can act as a disincentive to starting a business.

- Because the capital gains tax applies to the nominal return on capital, without adjusting for the fact that inflation may have substantially reduced its real value, long-term projects can be made to lose money (or lose even more money) through this tax alone.

- Canadian provinces where the capital gains tax is lower, like Alberta, Saskatchewan, and Newfoundland and Labrador, tend to have some of the highest household savings rates in the country. Conversely, high taxes and low or even negative household savings rates also tend to go together, as in Nova Scotia and Prince Edward Island.

Chapter 5 – The Corporate Income Tax and Entrepreneurship

- The fact that there is more than one corporate income tax rate creates a threshold effect whereby some companies split their activities in order to reduce their tax burden, using time and energy that could be devoted to more productive activities.

- In 2000, when the federal rate was much higher, 15% of companies filing as a “small business” limited their incomes in order to be able to remain in this tax category; in 2009, after the federal rate had been reduced and the income threshold raised, only 8.5% of companies did so.

- The corporate income tax reduces the reward associated with entrepreneurship by making companies less profitable, and also reduces the savings available for capital accumulation, since the non-distributed profits of companies are a form of savings.

- A study examining the effect of this tax in 17 European countries between 1997 and 2004 found that when the tax rate goes from around 30% to 27.5%, the business entry rate increases by 0.88 percentage points.

- Another study looked at 85 countries and found that a 10-percentage-point increase in this tax rate reduces the number of businesses per 100 people by 1.9, and the business entry rate by 1.4 percentage points.

- An American study looking at the number of patents filed for the 1990-2006 period found that two thirds of companies affected by a tax increase filed around 5% fewer patents in the two years following the hike.

- A Canadian study that looked at variations in provincial corporate income tax rates from 1977 to 2006 found that a reduction of one percentage point increases economic growth by 0.1 to 0.2 percentage points, and by deduction, reduces entrepreneurial activity as well.

Introduction

One of the challenges economists face is to resist the tendency to want to withdraw a whole range of phenomena from economic analysis and entrust these to psychology. Keynesianism, for example, explained investor confidence in terms of “animal spirits,” and the propensity to consume as one’s income varies with a “fundamental psychological law.”(1) To take another example, the debate surrounding taxes and regulations governing the consumption of sugar and of tobacco starts with the assumption that society suffers from a widespread lack of willpower.(2)

In the same way, many try to divorce entrepreneurship from any fiscal questions. According to them, entrepreneurship is basically a passion, and entrepreneurs start businesses out of love.

The problem with these arguments is that they are not really arguments; they are rather ways of ending the discussion before it has really begun. After all, “there’s no accounting for taste,” as the saying goes.

The Importance of Cost

Yet one of the fundamental aspects of economic analysis is that theories that use cost variations as a primary factor accounting for human behaviour provide better explanations than theories that ask us to accept a change in people’s tastes, preferences, or values as primary factors.

Having said this, it is far from obvious which public policies really stimulate entrepreneurship and reduce the cost of starting a business, just as it is not easy to evaluate the cost of risk-taking for an entrepreneur. The naïve vision would be to believe that government assistance always favours entrepreneurship. After all, if there is a transfer of money—or of risk—then a certain choice is certainly made less expensive. But is the choice that is actually encouraged the one that was supposed to be encouraged?

Reality is more complex because behaviours change in response to public policy changes. For example, we have to make sure that aid goes to the right people, which is to say to entrepreneurs who would not have launched their business without government help. We also have to make sure that entrepreneurs do not change their projects just to benefit from subsidies, which would be even worse. In such a case, we have not only failed to truly stimulate the creation of new businesses, but on top of this, we have imposed an additional constraint on entrepreneurs that diverts them from their primary function, which is to resolve societal problems, not to satisfy political objectives.

The question of taxation and how it influences the decision to start a business is sometimes avoided even more directly: The discussion is shut down by pointing out that entrepreneurs must do their part to finance the numerous missions of the government. Yet the problem is precisely that when there are fewer entrepreneurs, there is less economic growth and less prosperity with which to finance those missions. Even those whose main concern is to maximize government resources, come what may, have an interest in not asphyxiating entrepreneurs with disproportionate taxes.

This paper aims to provide a frank, open discussion, based on academic studies and data from respected sources, in order to examine more directly and deeply the fiscal measures that affect entrepreneurship.

Chapter 1 will explore government assistance that aims to stimulate entrepreneurship; Chapter 2 will look into the decision to become an entrepreneur; Chapter 3 will examine the effect of progressive taxation on entrepreneurship; Chapter 4 will look at the effect of the capital gains tax; and Chapter 5, the effect of the corporate income tax.

Notes

1. John Maynard Keynes, The Collected Writings of John Maynard Keynes, Royal Economic Society, 1978, pp. 114 and 161.

2. Mario J. Rizzo, “Behavioral Economics and Deficient Willpower: Searching for Akrasia,” Georgetown Journal of Law & Public Policy, Vol. 14, 2016, pp. 789-806.

The graphs (Click to enlarge)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|